Why ESG-linked loans are impacting construction finances

25 October 2021

Environment, social and governance-linked loans are fast entering the mainstream. But which construction industry companies are linking their finances to ‘green’ targets and why? Lucy Barnard finds out

It doesn’t take long for Geoff Doherty, chief financial officer at Kingspan to start talking about virtuous circles and environmental, social and governance targets.

Over the last decade, the Dublin-listed building materials manufacturer which specialises in high-performance insulation systems, has marketed itself heavily on its green credentials and the ambitious targets its sets itself to reduce energy consumption.

By setting itself ambitious environmental, social and governance (ESG) targets and then putting its efforts into achieving them, Kingspan boasts that it has saved the world the equivalent of 110 million barrels of oil over the last 25 years and radically altered its power use so that all of its operational energy comes from renewables.

Energy:

•Maintain net zero energy status

•Increase direct use of renewable energy to 60% by 2030

• Increase onsite generation of renewable energy to 20% by 2030

•Install solar PV systems on all owned facilities by 2030

Carbon:

•Net zero carbon manufacturing by 2030

•50% reduction in product CO2 intensity from primary supply partners by 2030

•Zero emission company cars by 2025

Circularity:

•1 billion PET bottles upcycled into manufacturing processes by 2025

•All Quadcore insulation to utilise upcycled PET by 2025

• Zero company waste to landfill by 2030

Water:

•5 active ocean clean-up projects by 2025

•100 million litres of rainwater harvested by 2030

And that’s before you start to talk about the new ESG targets the company has set out to achieve over the next ten years which include reducing its manufacturing carbon emissions to as close to zero as technically possible and to make insulation panels using discarded plastic bottles fished out of the oceans.

“ESG targets tangibly make a difference,” says Doherty. “Never before has there been a greater correlation between wider business performance and doing the right thing on climate change and socially.”

Kingspan’s green commitments

Over the years Kingspan’s environmental commitments and actions have attracted investment from specialist ethical funds. In September 2020 Kingspan raised €750 million through the sale of ‘green bonds,’ and the company’s shareholders include funds such as Baille Gifford and Norges Bank which aim to select stocks based on strong ESG principles.

In June, Kingspan went a step further, taking out a €700 million five-year loan with a syndicate of ten international banks which is built around its ESG targets. Under the terms of the loan, the company is able to borrow money at a more advantageous rate if it meets the targets it has set itself than if it does not.

“There is a virtuous circle of meeting the needs of customers who need energy efficient solutions, the attraction and retention of high-performance talent and the ESG objectives of other stakeholders and capital providers,” Doherty says.

And Kingspan is not alone. Businesses around the world including Nokia, Shell and Philips, are increasingly linking their loans to targets aimed at tackling the climate crisis and promoting a fairer society.

Kiloutou’s green loan

ESG loans are becoming more common in the construction industry too. In July, French construction equipment rental giant Kiloutou arranged a €10 million banking facility, linked to its performance on sustainability goals including investment in low-emissions equipment and the representation of women in its management. In May, UK contractor Wilmott Dixon agreed a £50 million sustainability-linked loan facility coordinated by HSBC with an interest rate which varies depending on the firm hitting a series of targets based around the firm’s net-zero carbon commitments. French contractor Eiffage agreed a €2 billion five-year ESG-linked loan with a syndicate of twenty institutions in 2019. And a number of other contractors including Skanska are aiming to take out ESG-linked facilities when they next refinance.

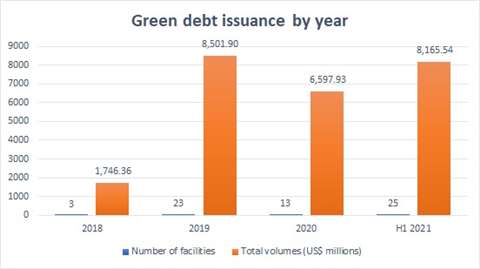

In fact, data specialist Refinitiv, calculates that ESG-linked loans issued to the construction sector in the first half of 2021 stood at US$8.1 billion, surpassing the US$6.6 billion issued by banks to the sector in 2020 and close to the US$8.5 billion issued to the sector throughout the whole of 2019. And the number of new ESG-linked loans issued by lenders to the sector increased to 25 in the first half of 2021, already surpassing the record 23 issued internationally in 2019.

“If you’d have asked me eighteen months ago, I would have said that our work in this area was occasional, focused among large, industrial corporates, and with ESG rarely being a key driver of the company’s refinancing strategy or the credit market’s appetite”, says Marc Finer, director for debt advisory at KPMG who specialises in plant hire financing and ESG-linked finance. “But today, nearly every conversation we have with our clients across every sector – and with all types of lenders - involves a discussion about ESG,”

Banks argue that businesses with clear ESG strategies are generally better run and less likely to default on their loans.

Sustainable constuction business

“Our starting point has always been that sustainable business is better business,” says Leonie Schreve, global head of sustainable finance at ING, which has been writing ESG-linked loans since 2017. “We see that companies with a credible sustainability strategy and strong sustainability practices have a lower credit risk. And having lower credit risk in our portfolio means we can price it differently.”

Unlike “green loans” where borrowings must be used for environmental projects or investments, ESG-linked loans have no restrictions on usage. Instead, the cost of debt is usually linked to three or four specific and measurable goals, often taken from a company’s own sustainability strategy. For example, Kingspan’s ESG targets comprise 12 specific targets surrounding the firm’s commitment to recycling and reducing energy and carbon. Under the loan agreement, if the company manages to meet these targets, the bank agrees to reduce the interest rate on the loan slightly.

“Linking financial products to the sustainability achievements of our clients is just another way we’re helping them to accelerate their sustainability agenda and really step up and make the changes they need to reach a net-zero commitment,” Schreve adds.

But that is only part of the story. Spurred on by Greta Thurnberg and a new generation of activists keen to take more drastic action to tackle climate change, shareholders around the world are putting pressure on banks to do more to demonstrate their commitment to saving the environment and promoting social change.

Greta Thunberg’s climate activism is influencing investors - photo: Reuters

Greta Thunberg’s climate activism is influencing investors - photo: Reuters

Earlier this year HSBC committed to set targets to reduce its exposure to carbon-intensive assets after a group of investors filed a resolution calling for the bank to curtail its financing of fossil fuels. And last year Barclays published a climate resolution plan after around a quarter of its shareholders supported a resolution requiring it to stop providing financial services to firms not aligned with the Paris climate accord.

Greta Thurnberg

The result is that at the moment, banks are particularly keen to sign as many ESG-linked loans as possible, meaning that companies which can secure such lending can get better terms (although the actual interest rate discount on loans usually amounts to only around 5-10 basis points).

Pressure from customers, employees and shareholders to commit to fighting climate change is also encouraging directors to sign up for something which looks like it may well soon be incorporated into the financial mainstream.

“For me, this is a business resilience issue and an access to capital issue,” Finer says. “Companies are focusing on ESG not only because it’s morally the right thing to do, it’s because they know their business may not be resilient in the long term if they don’t. Lenders are starting to prefer and target those businesses which are able to make ESG commitments. Customers, in some cases, are already preferencing products from companies that they perceive to have a better record on environmental or social issues. Employees are choosing to work for these companies and holding their employers to account on their ESG commitments.”

2021 ESG-linked loans

But, without some way for banks and others to police whether or not targets have been met, critics complain that the concept runs the risk of being reduced to little more than a marketing exercise.

According to data firm Reorg, nearly two thirds of ESG-linked loans written during the first quarter of 2021 do not require a third party to verify that ESG targets have been met. And, with companies able to choose their own targets, there is a risk that they will not choose particularly stretching ones.

ING’s Schreve agrees a lack of third party verification, but argues that it is up to the companies themselves to make sure that they take on these loans in the right spirit.

“It’s critical for sustainably-linked financing structures to be ambitious and address the most urgent challenges with maximum impact,” she adds. “Anything less won’t contribute to the herculean task of building a sustainable economy. While ‘greenwashing’ is not a term we would use, there is a risk of falling standards, particularly as this type of financing becomes more mainstream.”

“The credibility of the market relies on clients themselves being committed to their sustainability goals and a net-zero future,” she adds. “There’s always a risk that companies go for less-ambitious targets, which in turn affects the quality of the product and lessens its impact. “

Photo- Reuters

Photo- Reuters

Moreover, to combat the perception that borrowers were being allowed “to mark their own homework,” three industry associations representing bankers, law firms and underwriters in Europe, the US and Asia have revised their sustainability-linked loan principles earlier this year requiring borrowers to obtain independent external verification of their performance against the targets set.

In May a joint working group of the Loan Market Association, the Asia Pacific Loan Market Association and the Loan Syndications and Trading Association published an updated Sustainability Linked Loan Principles and accompanying guidance setting out voluntary market standards for what constitutes a sustainability-linked loan and how they should be assessed.

“The financial regulators are focussing on this area at present and looking carefully at how banks are monitoring claims to ESG credentials,” says Janine Alexander, a partner at law firm Collyer Bristow who specialises in financial market disputes. “Forthcoming changes in regulation and accountability are likely to mean that in future banks will demand more proof from borrowers that they have met the criteria set out and will be more prepared to act if they do not.”

“Borrowers should take legal advice before they sign up to any of these ESG-linked loans and think carefully about how they record progress against the targets/criteria set and be mindful of the reputational risk if it emerges they haven’t met or can’t prove they have met some of the targets they set themselves,” she adds.

Demand for scrutiny on ESG-linked loans

Demand for scrutiny for ESG-linked loans could spell more business for firms of external auditors which must already sign off on company accounts and loans. It is also prompting banks to take on expertise from the hundreds of ESG research agencies such as Sustainalytics and EcoVadis which help investors and consumers measure and benchmark a company’s ESG performance.

And, as well as holding borrowers to account over their targets, banks, and the ESG ratings agencies they use, are also starting to demand more stretching targets in the first place.

“The quality of debate we’re seeing lenders have with clients about their ESG commitments now is in a completely different zone to where it was eighteen months ago,” says Finer at KPMG. “Before, the bar was arguably lower in terms of what some lenders were prepared to accept. Now these do actually have to be commitments that are demonstrably really core and stretching.”

“If a plant hire company promises to remove all the plastic cups from the staff cafeteria. It’s not going to cut it,” he adds. “It would have to be something about the operations of that business like a commitment to transition their fleet to alternative fuel technology or to cut carbon emissions by a meaningful percentage. It has to be measurable. And it has to be benchmarkable. A bank will be looking at this plant hire company relative to five others and asking whether their commitment to cutting emissions is enough.”

Grenfell Tower

Yet critics still argue that the practice of linking such loans to just a few narrow ESG targets could well mean that wider issues are ignored.

Interestingly Kingspan signed its ESG-linked €700 million five-year loan with a syndicate of ten international banks in June 2021, several months after some of its biggest ethical funds shareholders were exiting their holdings in the company citing concerns over its governance.

Investors Janus Henderson, WHEB Asset Management, Pictet Asset Management and Guinness Funds said they had sold their stock in Kingspan over concerns about the culture of the business which emerged following evidence company officials gave to the Grenfell Inquiry in November 2020. Fellow investors Baillie Gifford and Liontrust Asset Management also reduced their stake in the company.

Grenfell Tower in London - photo courtesy of Reuters

Grenfell Tower in London - photo courtesy of Reuters

Although the ongoing inquiry heard that Kingspan only supplied around 5% of the cladding used in the London tower which burnt down in 2017 and had no role in its design, Kingspan executives admitted that the company had sold Kooltherm K15 insulation without telling customers that it had failed fire tests.

“We have concluded that we are unable to continue to invest in Kingspan,” Seb Beloe, head of research at WHEB Asset Management wrote in a note to investors. “We believe, that the culture within the UK business enabled – even encouraged – an attitude that prioritised commercial advantage over product safety. Furthermore, based on the evidence presented at the Inquiry and our knowledge of the business, this culture was at least tacitly endorsed by group management.

In a statement Kingspan said that it had “identified and apologised for process and conduct shortcomings” in its UK insulation business and that it had implemented measures to “ensure that there could be no recurrence and to reinforce our fire safety focus.”

Moreover, with demand for ESG-linked loans set to increase, more and more companies in industries often shunned by socially conscientious investors are hoping to take advantage of the financing opportunity.

In December oil giant Shell agreed a $10 billion US revolving credit facility co-ordinated jointly by Bank of America and Barclays linked to the company’s progress in reaching its short term net carbon footprint intensity target. In March 2021 US gold miner Newmont Corporation signed a US$3bn loan facility including a feature which will adjust the interest rate depending on the group’s sustainability performance. And in August 2021, it emerged that tobacco giant Philip Morris International published its own set of ESG targets in the hope of attracting green finance.

Company environmental records

“If a company has a poor or controversial track record on environmental or compliance issues, I think it’s right that the banks should probe that history when lending them money,” says Finer. “There is that question which says do you cut them off or hold them to account that they have learnt from what they’ve done in the past and they are transitioning to something new and better?

“Every business can be looked at through a whole range of different lenses. I think you have to be a realist and see that business is a diverse place. The world is not a perfect place however, there is a collective surge of willingness from business and in society to change like there never has been so this is an opportunity to get your stakeholders together and get everyone to back that change.”

MAGAZINE

NEWSLETTER

CONNECT WITH THE TEAM